Highlighted Articles

July 1, 2018

Highlighted Articles (Click on Home above to see all articles):

- Solving the Toxic Assets Problem during the Great Financial Crisis (Website) (PDF)

- The Economist magazine: The battle for Stuyvesant Town: The Housing Rubble (Economist Website) (PDF)

Management, Building and Growing a Business:

Creative Solutions/Ideas:

- A New Method for GSE Risk Transfer (PDF)

- Solving The Bad Asset Problem (PDF)

- How to Finance Clean Energy & Infrastructure Investments

- Tackling the US Unemployment Problem-Infrastructure Investments Without Increasing Taxes or Deficit

- Three Misconceptions about Issuer-Paid Ratings

- Rating Agency Reform – An Alternative for the Franken Amendment

- How Issuers can Increase Investor Interest in CMBS2 Mezz

- CMBS Hedging Requires a New Approach

- Restarting CMBS Lending

- Strategy for Tablets – What would Steve Jobs do at Microsoft?

- Leveling the Playing Field for Clean Energy & Infrastructure

Analysis & Comments on Markets & Economy:

- One Lesson from the Silicon Valley Bank Failure

- One Lesson for Investors from Brexit and Trump Victory Missed by Most

- What’s Ahead for US Interest Rates?

- Why have U.S. Interest Rates Defied Expectations and What Lies Ahead?

- Using Information Momentum to Understand Markets & Economy

- What’s Ahead for CMBS Spreads?

- What Do CMBS Spread Forecasts Say About Commercial Real Estate?

- Make Your Own Opinion About Commercial Real Estate

- Default Ruthlessness: Examining Borrower Default Behavior

- What’s Ahead for CMBS & Commercial Real Estate in 2013?

- Two Points For Investors

Tutorials:

Appeals:

Consider Helping Those Impacted by the Covid-19 Crisis: National Council for Behavioral Health COVID-19 Relief Fund, CDP COVID-19 Response Fund, and others.

Consider supporting our troops and their families – they have given so much: Special Operations Warrior Foundation, Wounded Warrior Project, and others

Note: Views expressed in my writings are solely my own.

See Also: Media Quotes, Market Comments, Some Useful Information

Using Information Momentum to Understand Markets & Economy

August 3, 2014

By Malay Bansal

A simple concept that is useful in understanding some counter-intuitive phenomena in markets and economy, and looking ahead to the future.

For over a decade, I have used a concept that I have called Information Momentum in my thinking and discussions to explain phenomena in markets and economy that otherwise do not seem completely intuitive. Understanding why something has been different from expected in the past also helps in understanding and looking ahead to what might happen in future.

At its core, the concept is simple and parallels the similar concept in physics. Every physical object has a mass, and if it is moving, it has a velocity. The product of the two is known as momentum. The higher the momentum, the greater the impact that object will have. The higher the momentum, the higher the force required to stop the object from moving or to change its direction.

A somewhat similar concept can be applied to information. In this case, consider the number of people who receive a new piece of information, and can act on it, as equivalent to the mass, and how fast people get this new information as equivalent to velocity. The more the number of people who receive the new information, or the quicker the new information reaches people, the higher the information momentum for that information.

The concept is simple and so are some observations which help apply the concept to understanding market behavior. Somewhat in jest, and continuing the parallel with physics, I have sometimes referred to them as my laws of information momentum. Four of these observations are mentioned below.

First law of Information momentum is that the information momentum will continue to increase with time. This is obvious today. It started increasing with with internet becoming more easily available to more people, first in US and then around the world. Then, each of the following, as it came on the scene, has contributed to a quantum jump in the information momentum: advent of the web (the world wide web), email, blogs, news sites, internet trading, faster connection technologies like DSL replacing old phone dial-ups, wi-fi connections everywhere, tablets & smartphones with data connection, twitter. This trend will continue and the increase in information momentum will magnify the impact of the other laws.

The second law is that higher information momentum means new information will have bigger impact than in the past. More people acting on a piece of information at the same time means bigger moves in market and possibly more often. A corollary to this law is that higher information momentum can, though will not always, increase volatility and correlation in markets.

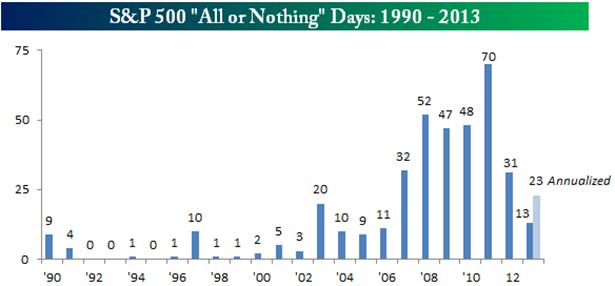

The observations by Bespoke Investment Group on “S&P 500 All or Nothing Days” (days where the net daily A/D reading in the S&P 500 exceeds plus or minus 400) as described in the article All or Nothing Days Becoming More Common Than Uncommon, and as shown in the chart below provide a good example of this over a long period.

Source: Bespoke Investment Group.

The third law is that more information momentum means better decisions will be made. Better decisions will logically lead to better outcomes, which in bigger picture, implies higher probability of higher profits for companies and better growth for the overall economy. All else being equal, the future will be better than the past. This applies at every level including at the level of individuals, companies, countries, local markets, and the entire world’s economy. At every level, decision makers will have access to more specific and detailed information and sooner than ever before. In addition to more detailed information about the specific situation, decision makers will have access to more ideas, viewpoints, opinions, suggestions, and criticisms from a wide variety of people through blogs, comments etc. As an example, in 2008 and 2009, when the economy worldwide was facing a huge crisis, with declining values of mortgage backed securities and other bad assets leading the biggest banks towards failure, and the government had to announce extraordinary measures like TARP, even people like me were able to chime in with suggestions directly to people at Treasury and Federal Reserve and via articles in New York Times etc (to toot my own horn, I suggested a plan involving public-private partnership – basically the concept behind TALF and PPIP programs announced and implemented several months later. See Solving The Bad Asset Problem or PDF).

It is easy to see that even with all else being equal, the future will be better than the past. But all else is not equal, if you look at things like what developments like search engines have done to personal and business productivity. You can find answers to almost any question you have just by googling it. Think about how Google Earth has changed the real estate businesses, and other similar examples. All of these are reasons to be optimistic about the future.

The fourth law states that since more information may become available with time, decisions will be made later in time, possibly at the last possible minute when they have to be made. At an earlier time, the Just-in-time concept significantly improved productivity in manufacturing. In a similar vein, decisions to act may be delayed till the last minute so as to take advantage of any additional information that may become available (what I call “Just-in-time decisions”).

Future articles will add more laws and give more specific examples detailing the application of these concepts for understanding various market and economic developments and looking ahead to the future (for the first example of application of these concepts, see Why have U.S. Interest Rates Defied Expectations and What Lies Ahead? ).

Note: The views expressed are solely and strictly my own and not of any current or past employers, colleagues, or affiliated organizations. My writings are simply expressions of my intellectual thought process. I welcome comments, observations, examples and any extensions of the concepts above.

What’s Ahead for CMBS & Commercial Real Estate in 2013?

January 12, 2013

By Malay Bansal

Why did CMBS perform well in 2012 and what lies ahead.

Note: These views were originally quoted on 19 Dec 2012 in article “Rally Drivers” in Structured Credit Investor. This article was also published on Seeking Alpha.

In 2012, the CMBS market had a significant rally as is evident from the table below showing bond spreads over swaps.

|

2011 Year End |

2012 Year End |

|

| GG10 A4 |

270 |

150 |

| CMBS2 Senior AAA (A4) |

120 |

90 |

| CMBS2 Junior AAA |

265 |

140 |

| CMBS2 AA |

400 |

180 |

| CMBS2 BBB- |

700 |

470 |

Not only were the spreads tighter significantly over the year, the performance was better than expectations by almost any measure. Issuance for the year was $48 Bn compared to forecast of $38 Bn. The new issue 10 year AAA spread to swaps ended at 90 compared to forecast of 140, and new issue BBB spreads ended at 410 compared to a forecast of 587 (all forecasts are averages of predictions by market participants as published in Commercial Mortgage Alert). The spread tightening was not limited to new issue either, legacy CMBS prices were up significantly too. Why did CMBS do better than expected, and can this trend of higher issuance and tighter spreads continue?

Why did Spreads Tighten?

There are two widely talked about reasons for spread tightening that generally apply to most of the spread products, and a third one that is specific to and very important for CMBS and commercial real estate.

First driver of spread tightening is the purchase of large amount of mortgage securities by the Federal Reserve under its quantitative easing programs and investors search for yield in this low yield environment.

Second significant factor is that the universe of spread product is shrinking as mortgage payoffs are greater than new issuance. $25-30 Bn of net negative supply per year in CMBS means that the money that was invested in CMBS is returned to investors and needs to be reinvested. More demand than supply leads to higher prices and tighter spreads.

The third factor is a chain reaction that is more interesting and significant. As the above two reasons lead to tighter spreads for new issue CMBS bonds, the borrowing cost for commercial real estate owners decreases. Lower debt service payments from lower rates mean they can get higher loan amounts on their properties. That means a lot of existing loans that were not re-financeable or were border-line and expected to default can now be refinanced and do not need to default. As more loans are expected to payoff and expected defaults decrease, investors expect smaller losses in legacy CMBS deals. That means tranches that were expected to be written off may be money good or have lower losses. So investors are willing to pay more for them, and as people move down the stack to these bonds with improved prospects, the result is tighter spreads for these legacy bonds. Lower financing cost resulting from tighter bond spreads also helps increase liquidity and activity in commercial real estate market as it allows more investors to put money to work at returns that meet their requirements. More activity in the real estate market leads to more confidence among investors and increases real estate values, further reducing expected losses in loans leading to even tighter bond spreads. This chain creates a sort of virtuous circle – the exact opposite of the downward spiral we saw in previous years when the commercial real estate market deteriorated rapidly.

Looking Ahead

As the virtuous cycle mentioned above continues, barring any shocks, spreads can continue tightening and lower financing cost from CMBS means that it can compete more with other sources of financing which means that CMBS volume can keep increasing. Indeed, the forecasts for CMBS issuance for 2013 generally range from $55 Bn to $75 Bn, up from $48 Bn in 2012.

Spreads, however, have less scope for tightening than last year in my view. Looking at historical spreads in a somewhat similar environment (see What’s Ahead for CMBS Spreads? April 4, 2011), CMBS2 AAA spreads could be tighter by 20 bps and BBB- by another 140 bps this year. Generally rising confidence in underlying assets should result in a flatter credit curve, which implies more potential for gains in the middle part of new issue stack. Spreads will move around. Given the unprecedented low yield environment, the search for yield by investors could drive spread slower than expected. At the same time, events in or outside US could cause unexpected widening. The market obviously remains subject to any macro shocks.

One concern cited by many investors is the potential loosening of credit standards by loan originators as competition heats up. That is a valid concern and if industry participants are not careful, history could repeat itself. However, though credit standards are becoming a little looser (LTVs were up to 75 in 2012 from 65-70 in 2011 and Debt Yields were down to 9-9.5% from 11% a year ago), we are nowhere close to where industry was in 2007. Still, investors should watch out for any occurrences of pro-forma underwriting if it starts to re-emerge.

Looking further ahead, maturities will spike up again in 2015-2017, with around US$100bn of 10-year loans coming due. This could cause distress, but hopefully the commercial real estate market will have recovered enough by then to absorb the maturities. Still, it is something that we need to be mindful of for next few years.

For me, one of the most important factors to watch out for is the continued supply of cheap financing for real estate owners. That has been one of the main factors that has brought us to this point from the depths of despair at the bottom and was the basis for programs like TALF & PPIP (see Solving the Bad Asset Pricing Problem) four years ago.

In the current low-growth and low-cap rate environment, investors cannot count on increase in NOI or further decrease in cap rates to drive real estate values significantly higher. That makes availability of cheap financing critical and much more important than historically for achieving their required rates of return to make investments.

Any disruption in availability of cheap financing can quickly reduce the capital flowing to real estate sector and may reverse the positive cycle that is driving spreads tighter and increasing real estate values. Anything that could reduce the availability of financing for commercial real estate owners will be the most important thing I will be looking out for this year other than the obvious factors.

In commercial real estate, hotels and multi-family have improved the most. Hospitality sector, with no long leases, was the first to suffer and among the first to gain as economy started improving. Multifamily sector has done well benefiting from the financing by GSEs. Office and retail sectors have seen increasing activity but face a high unemployment and low-growth environment. If the economy keeps improving at the current slow rate, I think the industrial sector will offer more opportunities and see more activity this year.

Note: The views expressed are solely my own and not of any current or past employers or affiliated organizations.

Solving The Bad Asset Problem

June 1, 2010

These suggestions, sent to the Treasury & FRB in Oct 2008, proposed a plan similar to the TALF and PPIP programs, months before Treasury and others came around to the idea. They were mentioned in the NY Times Executive Suite column by Joe Nocera (complete document is available at nytimes.com here). The Treasury plan was first announced by Treasury Secretary Tim Geithner on Feb 10, 2009. The writeup also included the Turbo concept of limiting interest payments and using excess interest to pay down loan principal, which was included in the TALF announcement on Legacy CMBS on May 19, 2009.

______________________________________________________________________________

Suggestions for Additional Steps for Tackling the Credit Crisis

By Malay Bansal

Oct 19, 2008

Several steps have been taken by the Treasury and Federal Reserve to address the current economic crisis. These are important and useful first steps, but as everyone knows, the problems are complex and will require additional action, including steps to tackle the root cause of the problem – declining house prices.

Obviously, any step to stabilize house prices will need to focus on decreasing supply by preventing foreclosures as much as possible, and increasing demand by providing incentives to new home buyers. Making mortgage payments more affordable is key to both. Most efficient will be approaches that help people on the margin – people on the verge of defaulting on their mortgage, or those considering buying a house.

Below are outlines of three suggestions I have for consideration along with other steps being contemplated:

1. Better use of part of TARP Funds targeted to buy mortgage assets: Treasury can partner with private buyers instead of buying assets itself.

- Will increase efficiency by tapping private funds. There is a lot of capital waiting to be invested in distressed assets, but has not been invested yet as prices need to be lower to achieve targeted returns without leverage.

- Treasury can lend to or partner with private buyers of distressed mortgage assets with terms like the following:

- Treasury will put up 50% and the private buyer will put up 50%, with Treasury’s interest being the senior interest.

- Funds will be used to buy distressed mortgages and securities at a discount from various large and small banks and financial institutions.

- Mortgage payments from purchased assets will be used in sequential order to (i) pay 5% interest to Treasury, (ii) 5% interest to the Private buyer, (iii) principal to Treasury, (iv) principal to the Private buyer, and finally (v) all residual to the private buyer as its return for the risk. This ensures that Treasury gets its money back first.

- The 5% interest for Treasury will apply for 5 years. After that, it will increase by 0.5% every year till it reaches 9%. Interest for private buyer will stay at 5%.

- Those taking the loan from treasury will need to agree to change mortgage terms to help homeowners including giving borrowers the option to (i) increase loan term by 5 to 10 years, and (ii) prepay loans at any time without penalty (any existing prepay penalties will be waived). Other terms to help homeowners may be included.

- Treasury will offer mortgage assets from banks for bids. The private buyer with the highest bid will get funds from Treasury. Banks will have option of accepting the highest bid or keeping the assets themselves.

- This type of plan will allow participation by numerous large and not-so-large investors. Since there will be multiple buyers competing to buy assets, with their own capital at risk, the plan would help in determination of fair market prices for distressed assets (instead of a situation in which TARP manager is the only buyer).

- This program can run in parallel with direct purchases of assets by treasury, or can be used to sell off assets purchased by Treasury at a future date.

2. Make mortgage principal payments tax-deductible for next 5 to 10 years.

- Mortgage interest is already tax-deductible. Making principal also deductible will make it easier for those who want to but are barely able to make their mortgage payments, and those who are considering buying a house.

- As an example, someone with a $350,000 mortgage and 28% marginal tax rate will save $6,250 over 5 years or $1,250/yr. Over 10 years, savings will be $14,900.

- Better than a single-shot stimulus payment, since (i) it will provide relief over a longer period of time, (ii) it attacks the root cause of the problem by targeting housing, and (iii) it will benefit local governments by preventing loss of property taxes that will otherwise result from foreclosure.

- The deduction may be limited to maximum 15 to 20% of total mortgage payment to focus the benefit more towards newer mortgages (after ten years, principal payment is likely to be more than 20% of total mortgage payment), &/or to mortgages issued in certain years to control total cost.

- The deduction can be phased out above a certain level of AGI to focus the benefit towards those who need it more.

3. Encourage mortgage modifications to lower monthly payments by extending the mortgage term by 5 to 10 years.

- Modify mortgages by increasing the term by 5 to 10 years to lower monthly payment. As an example, monthly payment on a 30 year mortgage with 6.5% rate will decrease by 4.4% (or $1,172/year on a $350,000 mortgage) if term is increased by 5 years. An increase of term by 10 years would reduce monthly payment by 7.4% (or $1,960/year on a $350,000 mortgage).

- Lowering payment without lowering interest rate may be more palatable from fairness perspective, and should be attractive to lenders if it avoids default. Removing any prepayment penalties should also be part of the modification as much as possible.

____________________________________________________

On Feb 10, 2009, Treasury Secretary Tim Geithner, in a much anticipated speech, announced the long-awaited toxic asset plan, but the market was disappointed by lack of details and sold off.

Extract from Treasury’s 10-Feb-2009 Fact Sheet on the Financial Stability Plan:

FACT SHEET

FINANCIAL STABILITY PLAN

1. Public-Private Investment Fund: One aspect of a full arsenal approach is the need to provide greater means for financial institutions to cleanse their balance sheets of what are often referred to as “legacy” assets. Many proposals designed to achieve this are complicated both by their sole reliance on public purchasing and the difficulties in pricing assets. Working together in partnership with the FDIC and the Federal Reserve, the Treasury Department will initiate a Public-Private Investment Fund that takes a new approach.

- Public-Private Capital: This new program will be designed with a public-private financing component, which could involve putting public or private capital side-by-side and using public financing to leverage private capital on an initial scale of up to $500 billion, with the potential to expand up to $1 trillion.

- Private Sector Pricing of Assets: Because the new program is designed to bring private sector equity contributions to make large-scale asset purchases, it not only minimizes public capital and maximizes private capital: it allows private sector buyers to determine the price for current troubled and previously illiquid assets.

NY Times Links:

http://graphics8.nytimes.com/images/blogs/executivesuite/posts/MalayBansalPlan.pdf

____________________________________________________

Solving the Bad Asset Pricing Problem

Note: This write-up was published on the Seeking Alpha here. It was a follow-up to the original suggestions, sent to Treasury & FRB in Oct 2008, which proposed a plan similar to the TALF and PPIP programs, months before Treasury and others came around to the idea.

By Malay Bansal

Feb 5, 2009

The Original TARP plan and the Aggregator Bad Bank ideas both have one major flaw: lack of a mechanism to determine appropriate prices for bad assets. Here is an approach to tackle this pricing issue. This approach also gets more bang for the buck for the Treasury by involving private capital in buying of these assets. More clarity in pricing and involvement of private investors are desperately needed for markets to return to normalcy.

There are already a lot of private investors who have raised significant amounts of money to invest in distressed assets. However, a lot of this cash has not been invested yet. Part of the reason is that they desire lower prices to get their returns to higher target levels than what they can get at present. Sellers, on the other hand, are often not ready to sell at even lower than current prices, especially when they believe that prices are already too cheap based on fundamentals. This has led to a stand-off which is leaving these assets on bank balance-sheets. So long as these assets stay on their balance-sheets and uncertainty about their prices continues, banks facing mark-to-market losses can not focus on restarting lending in these markets again.

Lower asset prices is one way private investors can get higher returns. The other method is if they can get financing for buying these distressed assets. If for example, they can get 50% financing on purchase price of assets, they can buy twice the amount of assets they could buy without the financing, thus roughly doubling their returns (minus the cost of financing). This will allow them to pay higher prices for assets and still earn their target returns.

In the current environment, financing is generally not available to investors in these assets. Given that financing can increase returns significantly, it is especially valued by investors at present. And that is what provides the solution to the pricing problem, and can ensure that the banks get the highest prices possible for these assets today, without the risk of any future Mark-To-Market (or actual) losses.

To attract private investors to buy distressed assets, the Treasury can offer to provide financing to private buyers. Prospect of higher returns, especially in an environment where returns on other assets are low, will attract lot of investors to the sector. However, financing will be provided to the buyer who has the highest bid on a given set of assets. That is important. The bidding process creates a mechanism for determining a fair market value for these assets. This plan will allow participation by numerous large and not-so-large investors, not just a few large investors selected by the Treasury. If the bid is too low and the bidder can make an exceptionally high return, another investor is likely to step in with a higher bid, if the bidding process is transparent and open to everyone. Different investors have expertise in different products. Those with the best expertise in the assets being offered will be able to value these assets and bid more aggressively. Since there will be multiple buyers competing to buy assets, with their own capital at risk, the plan would help in determination of fair market prices for distressed assets (instead of a situation in which TARP/Aggregator Bank manager is the only buyer). This bidding process also ensures the banks get the highest price possible for their assets in the current environment. If none of the bids are high enough, the bank is not required to sell, and can retain their assets. This ensures that banks are not forced by the program to sell assets at too low a price. If they choose to sell, their balance-sheet is cleared of these assets, and there is no future claw-back or liability related to these assets for them – the assets will be owned by a third party. They can go on to focus on other things.

Any cash flow received from the assets will be used first to pay interest to the Treasury and the private investors. Then, it will be used to pay principal back to the Treasury. Private investors will not get any of their principal back till Treasury has been paid back completely. The interest paid to private investors will be small (perhaps 4 to 5% range on their invested funds, not the face amount of securities) and will be meant to cover their expenses. Majority of their return will come at the back-end, their higher risk reflecting their higher returns. This priority for paying back Treasury funds first will protect public funds by decreasing the probability and amount of any potential losses on these assets.

Also, for home mortgage backed assets, Treasury can help homeowner mortgage-holders facing difficulty by requiring recipients of financing to agree to certain pre-specified steps to help homeowners in loan workouts.

Providing financing, instead of buying assets itself, provides more bang for the buck for the Treasury. As an example, if the Treasury offered 50% financing on AAA assets, and it has $100 Bn allocated to the program, the program will clear $200 Bn of assets from bank balance sheets. If the treasury used the funds to buy the assets itself, it will be able to remove only $100 Bn of assets from the banks’ balance sheets. Also, it reduces the risk of loss on these assets for public funds, since Treasury will be paid first and private investors will be bear the loss before the Treasury takes any hit.

Since private investors, who will have their own capital at risk before Treasury’s capital, will be buying and managing the assets, the Treasury will not need to build as big an infrastructure as it will need if it were to buy the assets itself. Nor will it need to pay management fees to third-party managers. Also, by using the private sector, this program can be ramped up much more quickly.

To achieve the highest rational prices, the bidding process must allow wide participation by large & small investors (bids should be requested for portfolio sizes that do not discourage small to medium size investors), amount and cost of financing should be known in advance of bidding (will likely be different for different pools and can be announced for each portfolio when it is put up for bid – treasury can even ask for multiple bids for different amounts of financing), and private capital must be at risk while protecting public funds (otherwise plan may face opposition from public).

I had originally included this suggestion among a few I had made to the Federal Reserve and Treasury officials in October after the original TARP plan was announced. I was happy to see the announcement of TALF, which will provide financing for new origination. However, financing for existing distressed assets will help clear the bank balance sheets of these assets, which is needed before banks are likely to increase originating new loans. Also, current Treasury plans do not include the Commercial Real Estate sector. It should be included before the issues in the sector escalate and become much bigger, as it will have significant impact on smaller regional banks that hold a lot of commercial real estate debt.

No single step will solve all the problems. Neither will this one, and it should be one of many approaches. But this approach can be effective since it will start the process for establishing prices for distressed assets, involving private capital in solving the problem, and cleaning up bank balance sheets, which are all prerequisites for eventual return to normalcy in the credit markets.

Fed’s Chicken-and-Egg Problem in CMBS & Two Suggestions on TALF

October 29, 2009

By Malay Bansal

Originators want to originate new loans, investors want to buy bonds with new conservatively underwritten loans, Treasury & Federal Reserve want the new issue CMBS market to start, borrowers certainly want to take out new loans to refinance maturing loans, and yet, four months after the Treasury launched the program, not one new issue CMBS deal has come to the market.

This highlights the chicken-and-egg type problem that the CMBS market faces. Everyone knows that the new origination will be of higher quality and so should have tighter spreads than the legacy bonds. Yet, lacking an efficient hedge, all that the originators have for indication of spreads are the legacy bonds, which are still too wide for new issue deals. In other words, originators are looking for tighter and stable bond spreads to originate, and market is looking for new collateral for tighter spreads – sort of a chicken-and-egg type problem.

One solution is to wait till legacy bond spreads tighten and stabilize, giving loan originators more confidence, but that might mean new issue TALF program may not get much traction before it ends. Another approach is to accelerate the legacy TALF program by removing some of the uncertainty that borrowers in that program face today. There are two easy to implement steps that will be helpful and allow investors to buy bonds throughout the month, rather than waiting till just before the TALF subscription date. First, the price used for calculating loan amount can be adjusted for interest rate movement from purchase date to the subscription date, and second, Federal reserve can allow potential borrowers to submit a list of potential bonds for purchase before actually buying the bonds, with approvals announced two or three weeks before the subscription date. Pre-approval of bonds will be almost as effective as disclosure by the Fed of their bond approval (or rejection) methodology, which more and more market participants are asking the Fed to do, and which Fed has been reluctant to do, probably because doing so might reduce their flexibility.

Note: A version of this article was published on Seeking Alpha.

Make Your Own Opinion About Commercial Real Estate

August 2, 2009

By Malay Bansal

Note: This write-up was published on Seeking Alpha website and was selected as an Editor’s Pick article.

Much has been written about the issues faced by Commercial Real Estate, extent of losses the CMBS bonds will sustain, whether the TALF, PPIP and other government programs will help, and if the commercial real estate market is showing signs of bottoming or is going to keep declining a lot more. There are various views which all seem plausible. If you are not professionally involved in real estate, or if you do not already have a definite view, how do you go about developing your own opinion? This article is an attempt to help with that process.

First step in the process is defining the problem being faced by the CRE market. It is a complex problem and yet the best description of it I have seen is a simple one sentence comment reportedly made by a panelist at a recent industry conference organized by CMSA:

“We have gone from a 6% Cap, 80% LTV world to a 8% Cap, 60% LTV world.”

That is another way of saying the CRE market faces a double-whammy of falling prices and reduced availability of debt, but the use of numbers in this short one sentence elegantly and succinctly captures the essence of the problem. A simple example will help explain.

Let’s take a commercial property, say an office. It is year 2006, property generates $600,000 in rental income per year, and cap rates are 6%. That results in value of $10 mm (600K/6%). In an 80 LTV world, Larry the Landlord buys the building for 10 mm, borrowing 8 mm (80% of 10 mm) for 5 years from a CMBS lender, and using 2 mm of his own money. Now fast forward to a time closer to loan maturity. In the new world, cap rates are 8%, so the new value is lower at 7.5 mm (600K/8%), and the new loan amount is 4.5 mm (60% of 7.5 mm). To refinance, Larry needs to pay off 8 mm, but can only get 4.5 mm in new loan. So, he needs to come up with 3.5 mm. If he has that money or can raise it from somewhere else, he can refinance the old loan and continue to own the property.

If Larry can not raise the additional amount, or if he does not think that it is economically worthwhile to do so, then the loan is foreclosed, and one option for the lender is to sell the property. Ideally, the property can be sold for 7.5 mm, the new value. In the worst case, there should be plenty of buyers at 4.5 mm (since one can buy the property no money down using the 4.5 mm debt available in the new world). The actual price will be somewhere between the two depending on how many buyers are there with cash available to buy, and what is their view of real estate prices in future.

By using the above numbers, we can quantify the range of expected losses in cases of sales:

| Decline or Loss | %Decline or Loss | |

| Property Prices | 2.5 to 5.5 mm | 25% to 55%. |

| Borrower’s Equity | 2 mm | 100% |

| CMBS debt | 500K to 3.5 mm | 6.25% to 43.75% |

If you layer in other factors, for example, if you assume that building’s cash flow decreases by 15% due to higher vacancy or lower rental rates (or the actual rent is lower than the assumed rent in aggressive underwriting), the numbers become worse:

New cashflow is 510 K, which results in new value of 6.375 mm, and new loan of 3.825 mm. With a new buyer paying something between 3.825 mm and 6.375 mm in case of a sale, the range of losses is:

| Decline or Loss | %Decline or Loss | |

| Property Prices | 3.625 to 6.175 mm | 36.25% to 61.75%. |

| Borrower’s Equity | 2mm | 100% |

| CMBS debt | 1.625 to 4.175 mm | 20.31% to 52.19% |

Broad ranges for sure, and you can quibble with the cap rates or LTVs, or the fact that this simple analysis ignores other expenses and complexities, but these are back-of-the-envelope numbers, and give you an idea. For CMBS deals, you also need an estimate on how many loans in a given deal will default. If you assume approximately 40% losses on defaulting loans, then defaults on 20% of loans in the pool will result in 8% losses on CMBS deals, which is somewhere in the middle of the range of losses being predicted by many of the market participants.

Loan extensions can postpone the problem, but not necessarily avoid it, unless the property prices go back to the old levels quickly, which no one expects.

Looking at the example above, one can clearly see the importance and impact of availability of debt. If debt up to 80 LTV were to become available again, that will narrow the ranges above significantly. Clearly, programs like TALF and PPIP that help increase availability of debt are helpful and important. But, they do not solve all problems. They do not help with the decline in value. That pain has to be taken, even though many are trying to ignore it. The current low transaction volume environment reduces confidence in valuations, but eventually volume and clarity on new valuations will both increase. Those who own commercial real estate property with a lot of debt and can not carry it through the downturn will suffer losses they have not recognized yet. But those who have cash and can buy properties at cheap levels in distressed sales will benefit. As always, it will be important to analyze and understand not just the sector, but the individual investments being considered.

What Would the TARP Public-Private Partnership Look Like?

March 16, 2009

By Malay Bansal

Note: This write-up was published on the Seeking Alpha website here.

On Feb 10, when the Treasury secretary Tim Geithner announced the Financial Stability Plan, which included a Public-Private Partnership Fund to remove bad assets from banks’ balance sheets, the markets reacted very negatively because of disappointment with lack of details on the plan. According to news items, the announcement of details is imminent now. Given the magnitude of reaction to the original announcement, many in the market await the plan details with interest.

That Fed should provide financing to private investors, instead of buying toxic assets itself (to help remove these troubled assets from banks balance sheets), is accepted by a lot more people now. By involving private capital, the government can minimize use of public funds and provide a mechanism for determination of fair prices for these toxic assets based on competitive bids by multiple private investors (my follow-up and original articles describe the reasoning).

Although no details have been announced, and the details are likely to change till the program is finalized, recent news articles have suggested that the administration is considering setting up multiple Investment Funds, with a Private Investment Manager running each fund. The Investment Managers will put up some equity, and government will provide financing to the funds. The private investment managers would run the funds, deciding which assets to buy and what prices to pay. Since there would be a limited number of funds, they would most likely target all types of assets rather than focusing on one specific type of distressed security. In addition to providing financing, government will also add equity to the fund alongside the private manager and would share in any gain or loss with the manager.

Even this simple description has couple of factors that are significant and bear watching.

First, if the government sets up a limited number of Investment Funds, it will reduce the competition for assets. One of the major results desired is for the selling banks to get the highest rational price possible for these assets to avoid further losses to them. With just five to ten investment funds bidding, the banks will be less likely to get the highest possible price. Instead of setting up just a few Investment Funds, the financing should be available to all investors – whoever has the highest bid on the legacy assets being sold should get it. Let various people and companies who have expertise in different types of assets assess and bid on them. Greater expertise and competition will result in higher sale prices.

Second, the idea of government putting in equity in these Investment Funds is less than ideal. The logic for doing this, of course, is that the private investors will benefit from the plan, and so the public should benefit too by investing alongside them. However, the goal of government in this endeavor is not to take investment risk for any potential gain, and Treasury should not be risking public money in this manner.

Also, saying that public should benefit alongside the private investors implies that the private investors are getting a sweet deal from the government and would make outsized returns by using government’s help. Suggesting this would only generate opposition to the plan from the public. Reality is, and should be, that the private investor should be taking the first loss risk. No public money should be at risk of loss till the private investor has been fully wiped out. This risk is what justifies the higher returns the private investors will get, if the asset performance does not turn out to be worse than pricing assumptions. Their returns will be less than expected if the asset performance is worse than assumed at the time of pricing. It will be very important to explain this aspect to lawmakers and general public to promote understanding and to avoid criticism and opposition of the plan. Private investors should not be asking the government for additional guarantees, and should clarify the risks they are taking to avoid backlash from general public and lawmakers.

Another justification offered for Treasury to put in equity in these funds may be to increase the total amount of funds used to buy toxic assets. Using simple numbers of let’s say 50% equity and 50% financing, the argument may be that, if the private investor puts $100 million, then government will put in another $100 mm resulting in total $200 mm of capital. If however, the government also put in $100 mm of equity alongside the $100 mm of private investor’s capital, then the total of $400 mm will be available to purchase assets. However, this logic is flawed. In this example, the government will be putting in $300 mm of capital and private investor $100 mm. If the government only provided financing, using the same 50% equity and 50% financing, it will be able to get total of $600 mm to purchase assets.

The TALF program has undergone significant changes since it was originally announced. In fact, the Public-Private Program could even be modeled along somewhat similar lines.

The Public-Private Partnership program will play an important role in the cleanup of bank balance sheets, which is one of the prerequisites for eventual return to normalcy for credit markets. We watch with interest what it would look like when the Treasury announces the details.

Geithner Announces Financial Stability Plan

February 10, 2009

By Malay Bansal

Treasury Secretary Tim Geithner announced the long-awaited toxic asset plan, but the market is disappointed by lack of details.

The plan is headed in the right direction but implementation details will be important.

Extract from Treasury’s 10-Feb-2009 Fact Sheet on the Financial Stability Plan:

FACT SHEET

FINANCIAL STABILITY PLAN

1. Public-Private Investment Fund: One aspect of a full arsenal approach is the need to provide greater means for financial institutions to cleanse their balance sheets of what are often referred to as “legacy” assets. Many proposals designed to achieve this are complicated both by their sole reliance on public purchasing and the difficulties in pricing assets. Working together in partnership with the FDIC and the Federal Reserve, the Treasury Department will initiate a Public-Private Investment Fund that takes a new approach.

- Public-Private Capital: This new program will be designed with a public-private financing component, which could involve putting public or private capital side-by-side and using public financing to leverage private capital on an initial scale of up to $500 billion, with the potential to expand up to $1 trillion.

- Private Sector Pricing of Assets: Because the new program is designed to bring private sector equity contributions to make large-scale asset purchases, it not only minimizes public capital and maximizes private capital: it allows private sector buyers to determine the price for current troubled and previously illiquid assets

Solving the Bad Asset Pricing Problem

February 5, 2009

Note: This write-up was published on the Seeking Alpha website here. It was a follow-up to the original suggestions, sent to Treasury & FRB in Oct 2008, which proposed a plan similar to the TALF and PPIP programs, months before Treasury and others came around to the idea.

By Malay Bansal

The Original TARP plan and the Aggregator Bad Bank ideas both have one major flaw: lack of a mechanism to determine appropriate prices for bad assets. Here is an approach to tackle this pricing issue. This approach also gets more bang for the buck for the Treasury by involving private capital in buying of these assets. More clarity in pricing and involvement of private investors are desperately needed for markets to return to normalcy.

There are already a lot of private investors who have raised significant amounts of money to invest in distressed assets. However, a lot of this cash has not been invested yet. Part of the reason is that they desire lower prices to get their returns to higher target levels than what they can get at present. Sellers, on the other hand, are often not ready to sell at even lower than current prices, especially when they believe that prices are already too cheap based on fundamentals. This has led to a stand-off which is leaving these assets on bank balance-sheets. So long as these assets stay on their balance-sheets and uncertainty about their prices continues, banks facing mark-to-market losses can not focus on restarting lending in these markets again.

Lower asset prices is one way private investors can get higher returns. The other method is if they can get financing for buying these distressed assets. If for example, they can get 50% financing on purchase price of assets, they can buy twice the amount of assets they could buy without the financing, thus roughly doubling their returns (minus the cost of financing). This will allow them to pay higher prices for assets and still earn their target returns.

In the current environment, financing is generally not available to investors in these assets. Given that financing can increase returns significantly, it is especially valued by investors at present. And that is what provides the solution to the pricing problem, and can ensure that the banks get the highest prices possible for these assets today, without the risk of any future Mark-To-Market (or actual) losses.

To attract private investors to buy distressed assets, the Treasury can offer to provide financing to private buyers. Prospect of higher returns, especially in an environment where returns on other assets are low, will attract lot of investors to the sector. However, financing will be provided to the buyer who has the highest bid on a given set of assets. That is important. The bidding process creates a mechanism for determining a fair market value for these assets. This plan will allow participation by numerous large and not-so-large investors, not just a few large investors selected by the Treasury. If the bid is too low and the bidder can make an exceptionally high return, another investor is likely to step in with a higher bid, if the bidding process is transparent and open to everyone. Different investors have expertise in different products. Those with the best expertise in the assets being offered will be able to value these assets and bid more aggressively. Since there will be multiple buyers competing to buy assets, with their own capital at risk, the plan would help in determination of fair market prices for distressed assets (instead of a situation in which TARP/Aggregator Bank manager is the only buyer). This bidding process also ensures the banks get the highest price possible for their assets in the current environment. If none of the bids are high enough, the bank is not required to sell, and can retain their assets. This ensures that banks are not forced by the program to sell assets at too low a price. If they choose to sell, their balance-sheet is cleared of these assets, and there is no future claw-back or liability related to these assets for them – the assets will be owned by a third party. They can go on to focus on other things.

Any cash flow received from the assets will be used first to pay interest to the Treasury and the private investors. Then, it will be used to pay principal back to the Treasury. Private investors will not get any of their principal back till Treasury has been paid back completely. The interest paid to private investors will be small (perhaps 4 to 5% range on their invested funds, not the face amount of securities) and will be meant to cover their expenses. Majority of their return will come at the back-end, their higher risk reflecting their higher returns. This priority for paying back Treasury funds first will protect public funds by decreasing the probability and amount of any potential losses on these assets.

Also, for home mortgage backed assets, Treasury can help homeowner mortgage-holders facing difficulty by requiring recipients of financing to agree to certain pre-specified steps to help homeowners in loan workouts.

Providing financing, instead of buying assets itself, provides more bang for the buck for the Treasury. As an example, if the Treasury offered 50% financing on AAA assets, and it has $100 Bn allocated to the program, the program will clear $200 Bn of assets from bank balance sheets. If the treasury used the funds to buy the assets itself, it will be able to remove only $100 Bn of assets from the banks’ balance sheets. Also, it reduces the risk of loss on these assets for public funds, since Treasury will be paid first and private investors will be bear the loss before the Treasury takes any hit.

Since private investors, who will have their own capital at risk before Treasury’s capital, will be buying and managing the assets, the Treasury will not need to build as big an infrastructure as it will need if it were to buy the assets itself. Nor will it need to pay management fees to third-party managers. Also, by using the private sector, this program can be ramped up much more quickly.

To achieve the highest rational prices, the bidding process must allow wide participation by large & small investors (bids should be requested for portfolio sizes that do not discourage small to medium size investors), amount and cost of financing should be known in advance of bidding (will likely be different for different pools and can be announced for each portfolio when it is put up for bid – treasury can even ask for multiple bids for different amounts of financing), and private capital must be at risk while protecting public funds (otherwise plan may face opposition from public).

I had originally included this suggestion among a few I had made to the Federal Reserve and Treasury officials in October after the original TARP plan was announced. I was happy to see the announcement of TALF, which will provide financing for new origination. However, financing for existing distressed assets will help clear the bank balance sheets of these assets, which is needed before banks are likely to increase originating new loans. Also, current Treasury plans do not include the Commercial Real Estate sector. It should be included before the issues in the sector escalate and become much bigger, as it will have significant impact on smaller regional banks,that hold a lot of commercial real estate debt.

No single step will solve all the problems. Neither will this one, and it should be one of many approaches. But this approach can be effective since it will start the process for establishing prices for distressed assets, involving private capital in solving the problem, and cleaning up bank balance sheets, which are all prerequisites for eventual return to normalcy in the credit markets.

_______________________________________________________________

Extract from my original Suggestions sent in Oct 2008 to the Treasury & the FRB (the write-up was mentioned in the NY Times Executive Suite column by Joe Nocera and the complete document is available at nytimes.com here). My writeup included the Turbo concept of using part of excess interest to pay down loan principal, which was included in the TALF announcement on Legacy CMBS on May 19, 2009).

——————————————

Suggestions for Additional Steps for Tackling the Credit Crisis

By Malay Bansal (malay.bansal@gmail.com)

Oct 19, 2008

2. Better use of part of TARP Funds targeted to buy mortgage assets: Treasury can partner with private buyers instead of buying assets itself.

- Will increase efficiency by tapping private funds. There is a lot of capital waiting to be invested in distressed assets, but has not been invested yet as prices need to be lower to achieve targeted returns without leverage.

- Treasury can lend to or partner with private buyers of distressed mortgage assets with terms like the following:

- Treasury will put up 50% and the private buyer will put up 50%, with Treasury’s interest being the senior interest.

- Funds will be used to buy distressed mortgages and securities at a discount from various large and small banks and financial institutions.

- Mortgage payments from purchased assets will be used in sequential order to (i) pay 5% interest to Treasury, (ii) 5% interest to the Private buyer, (iii) principal to Treasury, (iv) principal to the Private buyer, and finally (v) all residual to the private buyer as its return for the risk. This ensures that Treasury gets its money back first.

- The 5% interest for Treasury will apply for 5 years. After that, it will increase by 0.5% every year till it reaches 9%. Interest for private buyer will stay at 5%.

- Those taking the loan from treasury will need to agree to change mortgage terms to help homeowners including giving borrowers the option to (i) increase loan term by 5 to 10 years, and (ii) prepay loans at any time without penalty (any existing prepay penalties will be waived). Other terms to help homeowners may be included.

- Treasury will offer mortgage assets from banks for bids. The private buyer with the highest bid will get funds from Treasury. Banks will have option of accepting the highest bid or keeping the assets themselves.

- This type of plan will allow participation by numerous large and not-so-large investors. Since there will be multiple buyers competing to buy assets, with their own capital at risk, the plan would help in determination of fair market prices for distressed assets (instead of a situation in which TARP manager is the only buyer).

- This program can run in parallel with direct purchases of assets by treasury, or can be used to sell off assets purchased by Treasury at a future date.

My Suggestions on TARP

October 19, 2008

Note: These suggestions, sent to Treasury & FRB in Oct 2008, after the Treasury announced the original TARP plan to buy distressed assets, proposed a plan similar to the TALF and PPIP programs, months before Treasury and others came around to the idea. They were mentioned in the NY Times Executive Suite column by Joe Nocera and the complete document is available at nytimes.com here. The new Treasury plan was first announced by Treasury Secretary Tim Geithner on Feb 10, 2009. My writeup also included the Turbo concept of limiting interest payments and using excess interest to pay down loan principal, which was included in the later TALF announcement on Legacy CMBS on May 19, 2009. Another suggestion was to use tax incentives to increase housing demand.

By Malay Bansal

After TARP plan came out, I made some suggestions for improving it to the Treasury & Federal Reserve for their consideration.

My Suggestions included the following points:

- Treasury should provide financing to private buyers rather than buying distressed assets itself. Financing will help private buyers reach their target returns, and get them started on buying distressed assets clogging the system. Also, by providing financing to highest bidder on distressed assets, treasury will create a mechanism for pricing these assets based on competition from private buyers. Treasury can protect public funds by getting paid first and ensuring the private buyers get no more than 4 or 5% coupon (to cover expenses) on their invested money before the treasury gets its money back. Also, by requiring recipients to agree to certain steps to help homeowners, the plan can help homeowners who may be facing difficulty.

- Treasury will get the biggest bang for the buck by helping those on the cusp of defaulting, or those who may be considering buying a new home. Increasing home buying demand is as important as steps to decrease supply by reducing foreclosures. One step that will help more than a one-shot stimulus payment, will be to make the mortgage principal payments tax-deductible for next 5 to 10 or more years.

- One of the easiest steps to lower monthly mortgage payments will be to extend the mortgage term by 5 or 10 years for those facing potential problems. This should be least controversial of the modifications being discussed, and will not encourage those who do not need it to ask for it.

—————————————————————————————–

Suggestions for Additional Steps for Tackling the Credit Crisis

By Malay Bansal

Oct 19, 2008

Several steps have been taken by the Treasury and Federal Reserve to address the current economic crisis. These are important and useful first steps, but as everyone knows, the problems are complex and will require additional action, including steps to tackle the root cause of the problem – declining house prices.

Obviously, any step to stabilize house prices will need to focus on decreasing supply by preventing foreclosures as much as possible, and increasing demand by providing incentives to new home buyers. Making mortgage payments more affordable is key to both. Most efficient will be approaches that help people on the margin – people on the verge of defaulting on their mortgage, or those considering buying a house.

Below are outlines of three suggestions I have for consideration along with other steps being contemplated:

1. Make mortgage principal payments tax-deductible for next 5 to 10 years.

- Mortgage interest is already tax-deductible. Making principal also deductible will make it easier for those who want to but are barely able to make their mortgage payments, and those who are considering buying a house.

- As an example, someone with a $350,000 mortgage and 28% marginal tax rate will save $6,250 over 5 years or $1,250/yr. Over 10 years, savings will be $14,900.

- Better than a single-shot stimulus payment, since (i) it will provide relief over a longer period of time, (ii) it attacks the root cause of the problem by targeting housing, and (iii) it will benefit local governments by preventing loss of property taxes that will otherwise result from foreclosure.

- The deduction may be limited to maximum 15 to 20% of total mortgage payment to focus the benefit more towards newer mortgages (after ten years, principal payment is likely to be more than 20% of total mortgage payment), &/or to mortgages issued in certain years to control total cost.

- The deduction can be phased out above a certain level of AGI to focus the benefit towards those who need it more.

2. Better use of part of TARP Funds targeted to buy mortgage assets: Treasury can partner with private buyers instead of buying assets itself.

- Will increase efficiency by tapping private funds. There is a lot of capital waiting to be invested in distressed assets, but has not been invested yet as prices need to be lower to achieve targeted returns without leverage.

- Treasury can lend to or partner with private buyers of distressed mortgage assets with terms like the following:

- Treasury will put up 50% and the private buyer will put up 50%, with Treasury’s interest being the senior interest.

- Funds will be used to buy distressed mortgages and securities at a discount from various large and small banks and financial institutions.

- Mortgage payments from purchased assets will be used in sequential order to (i) pay 5% interest to Treasury, (ii) 5% interest to the Private buyer, (iii) principal to Treasury, (iv) principal to the Private buyer, and finally (v) all residual to the private buyer as its return for the risk. This ensures that Treasury gets its money back first.

- The 5% interest for Treasury will apply for 5 years. After that, it will increase by 0.5% every year till it reaches 9%. Interest for private buyer will stay at 5%.

- Those taking the loan from treasury will need to agree to change mortgage terms to help homeowners including giving borrowers the option to (i) increase loan term by 5 to 10 years, and (ii) prepay loans at any time without penalty (any existing prepay penalties will be waived). Other terms to help homeowners may be included.

- Treasury will offer mortgage assets from banks for bids. The private buyer with the highest bid will get funds from Treasury. Banks will have option of accepting the highest bid or keeping the assets themselves.

- This type of plan will allow participation by numerous large and not-so-large investors. Since there will be multiple buyers competing to buy assets, with their own capital at risk, the plan would help in determination of fair market prices for distressed assets (instead of a situation in which TARP manager is the only buyer).

- This program can run in parallel with direct purchases of assets by treasury, or can be used to sell off assets purchased by Treasury at a future date.

3. Encourage mortgage modifications to lower monthly payments by extending the mortgage term by 5 to 10 years.

- Modify mortgages by increasing the term by 5 to 10 years to lower monthly payment. As an example, monthly payment on a 30 year mortgage with 6.5% rate will decrease by 4.4% (or $1,172/year on a $350,000 mortgage) if term is increased by 5 years. An increase of term by 10 years would reduce monthly payment by 7.4% (or $1,960/year on a $350,000 mortgage).

- Lowering payment without lowering interest rate may be more palatable from fairness perspective, and should be attractive to lenders if it avoids default. Removing any prepayment penalties should also be part of the modification as much as possible.